📐 “Is Markov in the Room With Us?” — A Friendly Guide to Markov’s Inequality

A simple upper bound with powerful consequences in probability, risk, and algorithms.

🔍 Understanding Markov's Inequality: A Simple Bound in Probability Theory

Markov's Inequality is a foundational result in probability theory that gives a simple but powerful upper bound — even when we don’t know the full distribution of a random variable.

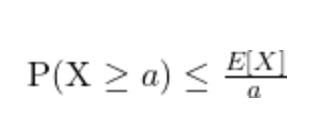

If X is a non-negative random variable, then for any $a>0a>0$:

$$

P(X \geq a) \leq \frac{E[X]}{a}

$$

🧠 Why It Matters

Markov’s Inequality tells us that if the expected value (or average) of a variable is small, the probability of it taking on a much larger value must also be small.

This is incredibly useful when:

We lack full knowledge of the distribution.

We want to rule out large deviations in value.

📊 Example

Suppose the expected value is:

Then:

There’s at most a 10% chance that XX is 100 or more.

📦 Applications

Markov's Inequality shows up in many places, including:

🧮 Algorithm analysis (e.g., performance guarantees)

📉 Risk modeling (e.g., bounding rare events)

🤖 Machine learning theory (e.g., generalization bounds)

📊 Statistical learning and data science

It also lays the groundwork for more advanced tools like Chebyshev's Inequality and Chernoff Bounds.

📎 P.S. Yes, Andrey Markov is very much in the room—at least when you’re thinking about bounds.